Nigeria’s digital lending landscape is poised for significant change as open banking moves closer to full implementation. This shift could reshape how credit is priced, how lenders assess borrowers, and how millions of Nigerians access formal financial services.

In a recent conversation with industry executives and sector analysts, insights emerged on how open banking can change Nigeria’s credit ecosystem while deepening financial inclusion. Central to this discussion is the bold vision of FairMoney Microfinance Bank, a lender that last year disbursed more than ₦150 billion in loans and paid over ₦7 billion in savings interest to customers.

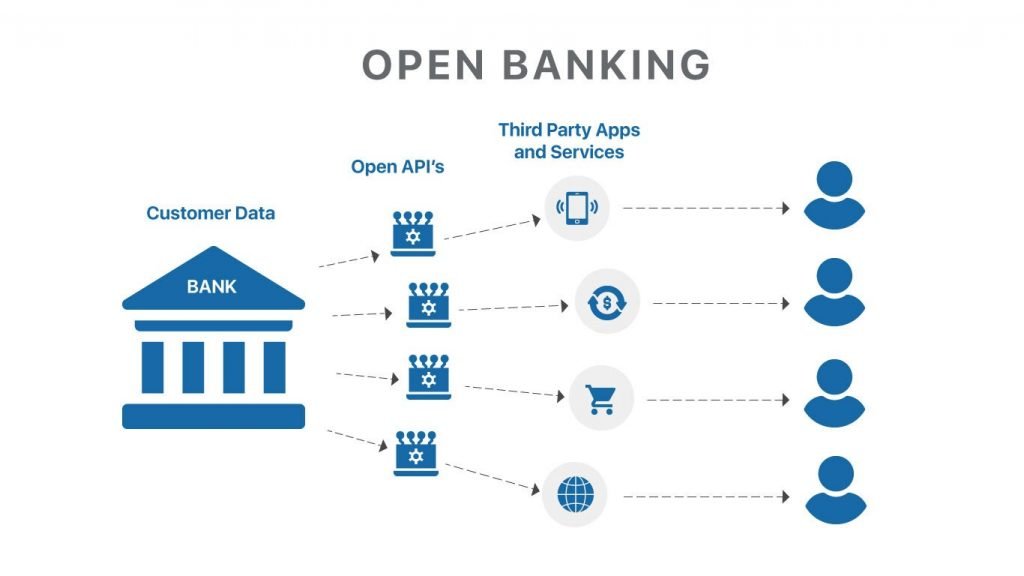

Open banking refers to a regulated framework where financial institutions share customer financial data with licensed third parties securely via application programming interfaces (APIs). The initiative aims to reduce friction in accessing financial data, improve creditworthiness assessments, and foster greater competition among lenders. Recent moves by the Central Bank of Nigeria to accelerate open banking rules, including plans for regional passporting agreements with other African countries, signal a strong regulatory commitment to this approach.

People who borrow today through digital platforms often face high interest rates because lenders have limited insight into their true financial behaviour. With open banking, lenders will be able to view a borrower’s payment history, savings patterns, and overall financial picture in real time. That could lead to more tailored loans and fairer pricing.

Industry leaders argue that this kind of transparency will create a more vibrant and responsible credit market. Rather than applying the same high rate to all borrowers, lenders will be able to match pricing to actual risk. This will help reduce the cost of credit for lower-risk customers while maintaining responsible credit standards for the broader market.

The Journey of Digital Lending in Nigeria

Nigeria’s fintech evolution has been rapid. When some digital lenders launched their platforms nearly a decade ago, the goal was simple: provide Nigerians with quick access to credit where traditional banks had limited reach. These early digital lenders helped millions of borrowers who lacked access to formal banking services.

Over time, financial technology firms started offering more than just credit. Savers now have access to deposit accounts, fixed deposits, debit cards, and payment solutions all through the same platforms that once offered only short-term loans.

FairMoney’s growth reflects this transformation. After starting as a digital lender, the company evolved into a fully-licensed microfinance bank regulated by the Central Bank of Nigeria. Its wide range of digital products now serves individual and business customers alike.

The broader digital lending market in Nigeria has also grown significantly. Data from industry reports show a clear rise in credit to the private sector over recent years, partly driven by fintech lenders. More players have entered the space, ranging from large tech startups to smaller specialised credit providers. Regulators have increased their oversight to ensure ethical practices and protect consumers.

This expanded market has not only boosted financial inclusion but has also helped Nigeria’s economy by making more credit available to small businesses and consumers outside the reach of traditional banking. With digital lenders disbursing billions of naira in loans each year, access to credit is no longer limited by branch location or formal employment status.

How Open Banking Could Reduce the Cost of Credit

One of the most talked-about impacts of open banking is its potential to lower the cost of borrowing. Interest rates in Nigeria’s digital lending market have often been high, reflecting the uncertainty lenders face when assessing risk. Without comprehensive customer data, lenders often charge a standard premium to cover potential defaults.

With open banking, lenders will have a clearer picture of an applicant’s financial behaviour. This includes bank balances, transaction history, savings consistency, and how borrowers interact with other financial products. Using this richer data, lenders can better segment customers by credit risk.

For example, someone with a steady income, regular savings, and good repayment history can be classified as a lower-risk borrower. The lender can then offer this person a loan at a more competitive interest rate. Conversely, borrowers with unstable income or inconsistent financial records will still be assessed carefully, but they will not be grouped together with lower-risk customers in the same cost band.

This approach benefits both lenders and borrowers. Lenders reduce default risk and improve decision accuracy while borrowers with strong financial habits are rewarded with fair pricing.

Experts point out that open banking itself does not directly reduce interest rates. Rather, the improved access to financial data empowers lenders to price credit more accurately. Over time, this accurate pricing is expected to bring down the average cost of credit in the market, encouraging more people to access formal financial services.

Open banking also supports innovation. Third-party developers can create new credit scoring models, budgeting tools, and financial planning apps that help borrowers improve their credit profiles. These innovations can further reduce perceived risk and expand access to fair credit.

Challenges and the Road Ahead

While the promise of open banking is significant, challenges remain on the path to full adoption. Technical infrastructure needs to be harmonised across banks, fintechs, and data providers. Security and data privacy must be top priorities to ensure customer information is protected at all times.

Another challenge is encouraging all financial institutions, big and small, to participate in data sharing. Smaller banks and microfinance institutions may lack the technology needed to connect quickly to open banking frameworks. The Central Bank and industry bodies are working to address these gaps by offering guidelines and support to participants.

There is also the issue of customer trust. Many Nigerians are still sceptical about sharing their financial data, even when the process is secure and regulated. It will take consistent education efforts for customers to understand the benefits of open banking and how it can improve their access to credit, savings, and financial planning tools.

As open banking implementation accelerates, regulators and industry stakeholders are expected to collaborate closely. Plans to issue an implementation roadmap within months show a renewed sense of urgency among policymakers and fintech leaders.

In the meantime, lenders like FairMoney are already preparing for the shift by building capabilities that integrate open banking data into their credit models. By doing this, they aim to offer more personalised products, reduce risk exposure, and support better outcomes for customers and the economy.

Nigeria’s drive towards financial inclusion has made notable progress. Yet nearly a quarter of adults still remain outside formal banking systems. The expansion of digital lending, backed by open banking frameworks, could play a pivotal role in reducing this gap.

A more inclusive financial system means more Nigerians can save securely, borrow responsibly, and build a financial history that unlocks broader economic opportunities. Access to tailored credit can boost consumer spending, help small businesses grow, and support national goals such as creating jobs and expanding economic participation.

Every step towards open banking brings Nigeria closer to a financial environment where credit is fairer, more transparent, and based on real data rather than guesswork. As fintechs, traditional banks, and regulators work together, the future of digital lending in Nigeria looks promising.

Join Our Social Media Channels:

WhatsApp: NaijaEyes

Facebook: NaijaEyes

Twitter: NaijaEyes

Instagram: NaijaEyes

TikTok: NaijaEyes